Florida Bankruptcy Exemptions: Complete Guide for 2026

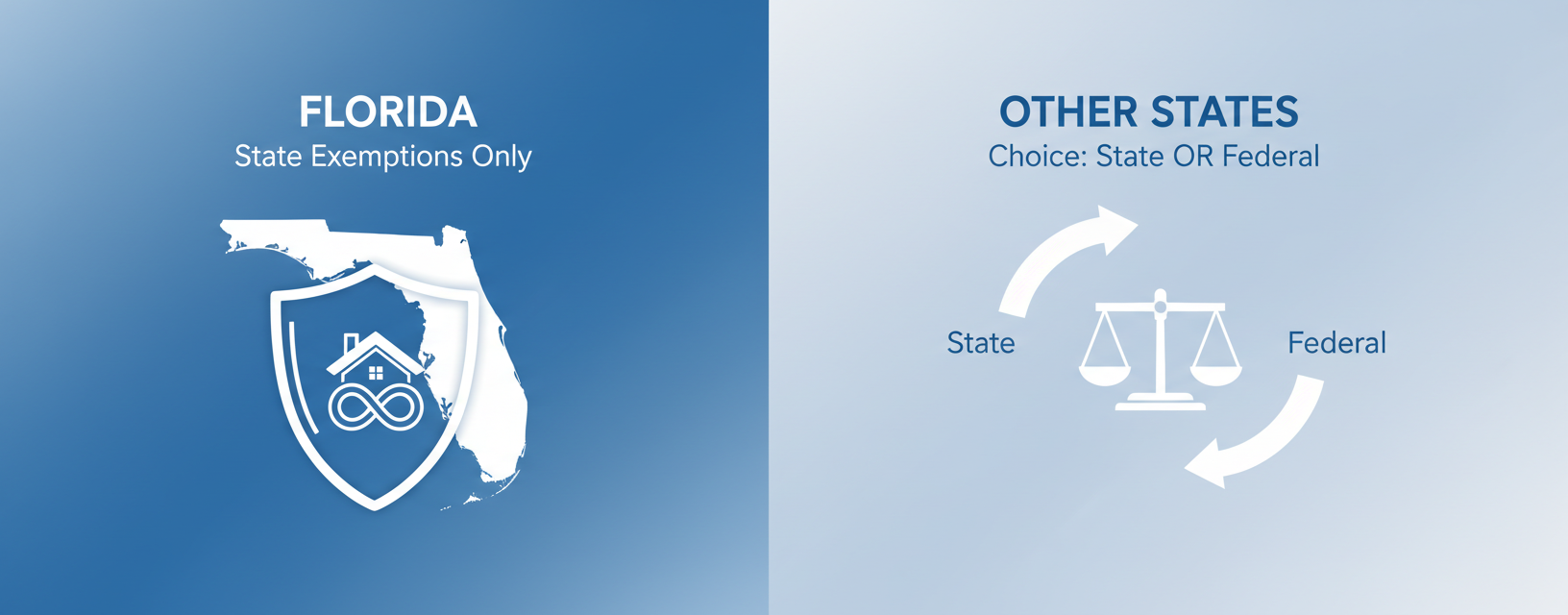

Most people filing bankruptcy in Florida don't realize they're working with a completely different set of rules than filers in neighboring states. You can't choose between state and federal exemptions here because Florida opted out of that choice to preserve its unlimited homestead protection. Florida's bankruptcy exemptions are generous for homeowners but have strict timing requirements, and understanding these details before you file can mean the difference between keeping your assets and losing them to the trustee.

TLDR:

- Florida requires you to use state exemptions only and blocks federal options

- Homestead exemption protects unlimited equity if you've owned your home 1,215+ days

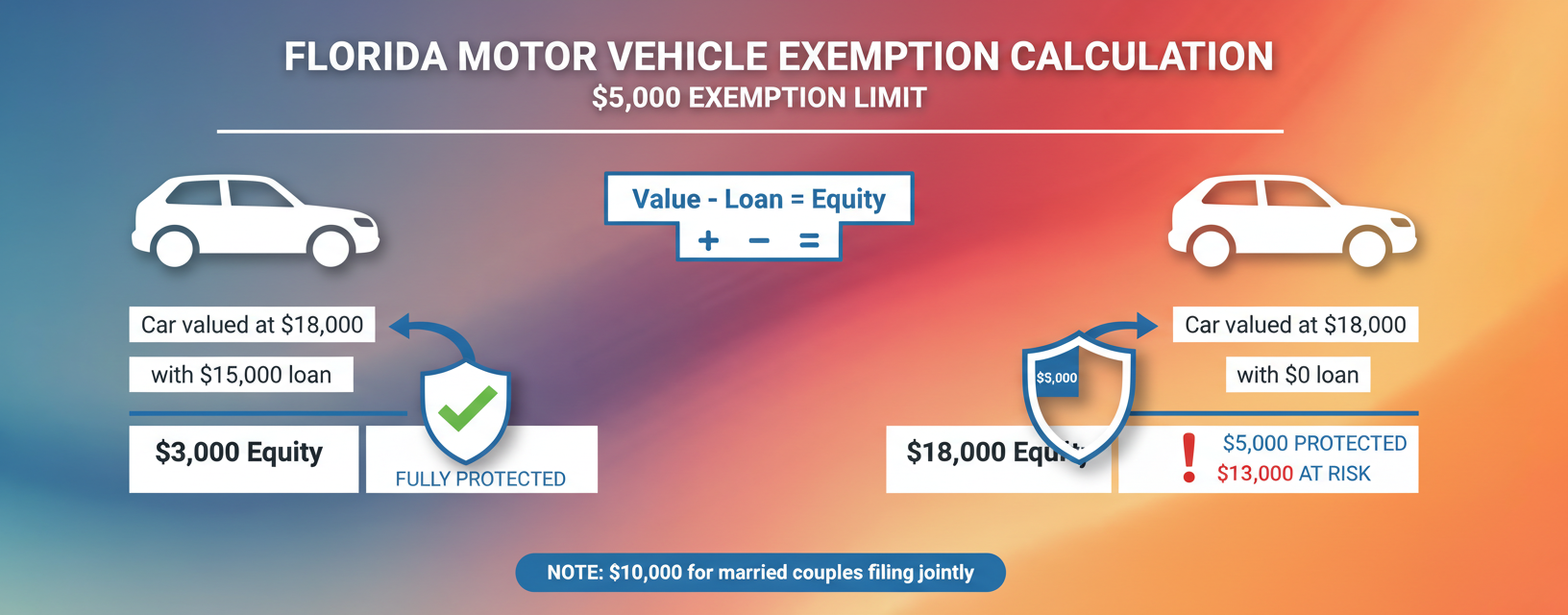

- Vehicle exemption covers $5,000 in equity; married couples filing jointly can protect $10,000

- Renters get a $4,000 wildcard exemption to protect cash, accounts, or other personal property

- Glade automates Florida exemption calculations and displays statute citations for every asset

Florida's Opt-Out Status: Why You Can't Use Federal Exemptions

Florida exercised its right to opt out of federal exemptions under 11 U.S.C. § 522(b)(2). If you file bankruptcy in Florida, you must use state exemptions only.

This differs from states like New Jersey or Connecticut, where filers choose between state or federal exemptions. Florida eliminated that choice to preserve its unlimited homestead protection. The federal homestead exemption caps at $27,900 per person, while Florida's has no dollar limit.

This benefits homeowners but may limit protection for filers with substantial personal property and no real estate.

Florida Residency Requirements for Bankruptcy Exemptions

Florida requires 730 days of residency before you can claim its exemptions. If you've lived here for less than two years, you'll use exemptions from whichever state you resided in for most of the 180 days before that 730-day lookback period.

Someone who moved to Florida 18 months ago from Georgia would need to use Georgia's exemptions. Federal exemptions apply only when timing issues prevent you from qualifying under any state's rules, which happens rarely.

Florida Homestead Exemption: Unlimited Protection for Your Primary Residence

Florida's homestead exemption protects unlimited equity in your primary residence. A $2 million home with no mortgage can be kept in Chapter 7 bankruptcy if you meet the requirements.

The property must be your primary residence and cannot exceed half an acre within a municipality or 160 acres outside city limits. You must have owned it for at least 1,215 days before filing. Properties owned for shorter periods face a federal cap of $214,000 on equity protection.

Investment properties, vacation homes, and rental properties receive no homestead protection.

Motor Vehicle Exemption in Florida Bankruptcy

Florida protects up to $5,000 in equity in one motor vehicle under Florida Statute 222.25. This covers cars, trucks, motorcycles, and other personal transportation vehicles.

Equity equals your vehicle's current market value minus any loan balance. A $18,000 car with a $15,000 loan has $3,000 in equity and remains fully protected. A $18,000 car with no loan has $18,000 in equity, leaving $13,000 unprotected.

Married couples filing jointly can stack exemptions to protect up to $10,000 in a shared vehicle. Each spouse claims their $5,000 against the same car.

If equity exceeds the exemption, outcomes vary by chapter. Chapter 7 trustees may sell the vehicle, return your $5,000, and pay creditors the remainder. Chapter 13 lets you keep the car but requires paying the excess equity through your repayment plan over three to five years.

Florida's Wildcard Exemption: Extra Protection When You Don't Use Homestead

Florida's wildcard exemption operates on a two-tier structure under Florida Statute 222.25. Every filer can protect $1,000 of any personal property they choose. If you don't claim the homestead exemption, that amount increases to $4,000.

Renters and filers without real estate automatically qualify for the $4,000 wildcard. Married couples filing jointly can double the wildcard, protecting up to $8,000 in personal property.

The wildcard covers anything you choose: cash, bank accounts, jewelry, electronics, collectibles, or any other asset not already protected by another exemption. You might use it to cover excess vehicle equity, wedding rings, or checking account balances.

Protected Retirement Accounts and Pensions Under Florida Law

Florida offers broad protection for retirement savings. ERISA-qualified plans like 401(k)s, 403(b)s, and pensions receive full protection under both federal and state law.

IRAs are also fully protected under Florida Statute 222.21, covering traditional IRAs, Roth IRAs, SEP IRAs, and SIMPLE IRAs. Florida has no dollar limits on IRA exemptions, unlike the federal IRA cap of approximately $1.5 million.

Public employee pensions receive unlimited protection, including retirement benefits for teachers, firefighters, police officers, and state and county employees. If your retirement account qualifies for federal tax exemption under the Internal Revenue Code, Florida treats it as fully exempt from creditors during bankruptcy.

Wage Protection for Heads of Household

Florida Statute 222.11 protects wages for heads of household from creditors during bankruptcy. The exemption covers the greater of $750 per week, 75% of your disposable earnings, or 30 times the federal minimum wage.

Head of household means you provide more than half the financial support for a dependent. This includes your child, spouse, parent, or other relative you're legally or morally obligated to support. You don't need to be married or have children.

The protection covers earned wages not yet paid and wages deposited into your bank account within the past six months. In Chapter 13, protected wages cannot be counted toward what creditors receive through your repayment plan.

Chapter 7 vs. Chapter 13: How Exemptions Work Differently

Chapter 7 is for filers who can't repay their debts. If you have nonexempt property, the trustee can sell it and distribute proceeds to creditors. Most Chapter 7 filers have no nonexempt assets.

Chapter 13 requires a three- to five-year repayment plan. You keep all property, but nonexempt asset values set your minimum payment. If you have $15,000 in nonexempt property, your repayment plan must pay creditors at least that amount.

Some filers who qualify for Chapter 7 choose Chapter 13 to prevent foreclosure or repossession, allowing them to catch up on missed payments.

Common Exemption Mistakes Florida Filers Make

Misvaluing assets is the most frequent error. Filers often use purchase prices instead of current market value, which can leave property unprotected or raise trustee concerns.

Missing the 1,215-day homestead ownership requirement limits equity protection to $214,000. Filers who recently purchased homes or moved to Florida often overlook this timing rule.

Improperly claiming the wildcard exemption happens when filers use the $4,000 amount while also claiming homestead. You only get the larger wildcard if you skip homestead protection entirely.

How Glade AI Simplifies Florida Bankruptcy Exemption Calculations

Glade's exemptions agent applies Florida bankruptcy exemptions automatically when building schedules. The system identifies your filing district and matches the correct exemption statutes to each asset category.

Every exemption shows its statute citation and reasoning. You can override any automated selection when your case requires a specific exemption strategy. The agent handles statute matching while you control the legal decisions.

This saves time on routine cases without hiding how exemptions are determined.

Final Thoughts on Understanding Florida Bankruptcy Exemption Rules

Your exemptions determine what you keep and what you might lose when filing bankruptcy in Florida. The state's bankruptcy exemption system protects major assets if you apply the rules correctly, from unlimited homestead equity to full retirement account protection. Small errors in valuation or timing can turn protected property into nonexempt assets, which is why accuracy matters from your first filing. Getting exemptions right the first time keeps your case moving forward without surprises or complications.

FAQ

How long do I need to live in Florida to use its bankruptcy exemptions?

You must be a Florida resident for at least 730 days (two years) before filing bankruptcy to claim Florida's exemptions. If you've lived here for less than two years, you'll use exemptions from the state where you resided for most of the 180 days before that 730-day period.

Can I protect my car if I still owe money on it?

Yes, Florida protects up to $5,000 in vehicle equity. Your equity is the car's current market value minus any loan balance. A $18,000 car with a $15,000 loan has only $3,000 in equity, which is fully protected. Married couples filing jointly can stack exemptions to protect up to $10,000 in one vehicle.

What happens if I recently bought my Florida home?

If you've owned your Florida home for less than 1,215 days before filing bankruptcy, your homestead protection caps at $214,000 in equity. After that 1,215-day period, Florida's unlimited homestead exemption applies, protecting your entire primary residence regardless of value.

Do I get the $4,000 wildcard exemption if I own a home?

Only if you don't claim the homestead exemption on that home. Florida gives everyone a base $1,000 wildcard, which increases to $4,000 if you skip homestead protection. Renters and people without real estate automatically qualify for the $4,000 amount.

Are my retirement accounts protected in Florida bankruptcy?

Yes, Florida fully protects ERISA-qualified plans like 401(k)s and pensions, plus all types of IRAs (traditional, Roth, SEP, and SIMPLE) with no dollar limits. Public employee pensions for teachers, firefighters, police officers, and state workers receive unlimited protection.